Managing rental properties without clear financial tracking can lead to costly mistakes. Monthly rental property reports help landlords monitor income, expenses, and overall property performance. These reports are essential for making informed decisions, simplifying tax preparation, and spotting potential issues early.

Key Takeaways:

- What’s Included: Income and Expense Statements, Rent Rolls, Account Ledgers, and Owner Statements.

- Why They Matter: Track rent collection, control expenses, and optimize cash flow.

- Metrics to Monitor: Collection rate (aim for 95%+), Net Operating Income (NOI), and reserve balances.

- Practical Tips: Organize reports by property and date, review them monthly, and use them to prepare for taxes.

Landlords can use these reports to better manage their investments, identify trends, and ensure financial transparency.

Core Components of Monthly Rental Property Reports

When it comes to managing rental properties effectively, having access to detailed and accurate reports is essential. A monthly rental property report isn’t just a single document – it’s a collection of interconnected statements that provide a comprehensive view of your property’s financial health. Each component plays a role in helping property owners make informed decisions and analyze performance thoroughly.

Standard Income and Expense Statement

This statement serves as the foundation of your monthly report, summarizing key financial details. It starts with basic property information, such as the reporting period, property address, unit details, and owner information. From there, it breaks down financial activity:

- Income: Includes gross rent (with dates), late fees, pet rent, utility reimbursements, and any non-sufficient funds (NSF) fees.

- Expenses: Covers management fees (usually 8%–10% of collected rent for long-term rentals), maintenance costs (with vendor names and invoice numbers), operating expenses like insurance and HOA dues, and leasing commissions.

"If your property manager’s monthly statement requires a phone call to understand, the statement isn’t doing its job." – Peter Lohmann, CEO, RL Property Management

The statement concludes with two critical figures: the net disbursement (the amount transferred to your bank account) and the ending cash balance, which becomes the starting balance for the next month. Most professional reports follow a cash basis accounting method, recording income when received and expenses when paid. This summary sets the stage for the more detailed breakdowns found in sub-ledger reports.

Sub-Ledger Reports

Sub-ledger reports provide in-depth details that go beyond the standard income and expense summary. These reports include:

- Rent Roll: Tracks scheduled rent, payment status, and any vacancy days.

- Account Ledger: Logs every transaction, including dates, categories, and running balances.

- Maintenance Sub-Ledger: Breaks down work orders by unit, listing vendor details, descriptions of the work performed, and invoice numbers.

"A single ‘Maintenance: $342’ entry is not enough information to verify the work happened or was priced fairly." – Peter Lohmann, RL Property Management

These reports aren’t just for record-keeping – they’re tools for analysis. For instance, cross-referencing the rent roll with the income statement can quickly highlight discrepancies between scheduled and collected rent. Similarly, reviewing maintenance sub-ledgers over time can help identify recurring issues in specific units, which might signal the need for larger repairs or replacements.

"The rent roll is your property’s financial roadmap – it tells you where you are today and what’s coming." – 1 Realty Management

Trust Account and Reserve Balances

Trust accounts and reserve balances are key components of financial transparency and preparedness. A trust account is a separate bank account where property managers hold funds like collected rents and security deposits, keeping them separate from their operating funds. For example, in Florida, security deposits must be held in a Florida-based account and should not be included in your disbursable cash balance.

The reserve fund serves as a financial buffer for routine repairs and minor emergencies. Managers typically set a minimum reserve amount (often $500 for a single-family home) and replenish it using incoming rent when the balance dips below the threshold. Every withdrawal and subsequent replenishment should be clearly documented.

"Your reserve is your money. Drawdowns and replenishments should be documented like any other line." – Peter Lohmann, RL Property Management

It’s crucial to ensure the ending balance of the trust account and reserve fund matches the starting balance for the next month. Any unexplained discrepancies – such as a reserve fund dropping from $500 to $120 without proper documentation – should be investigated immediately.

sbb-itb-73b3b1a

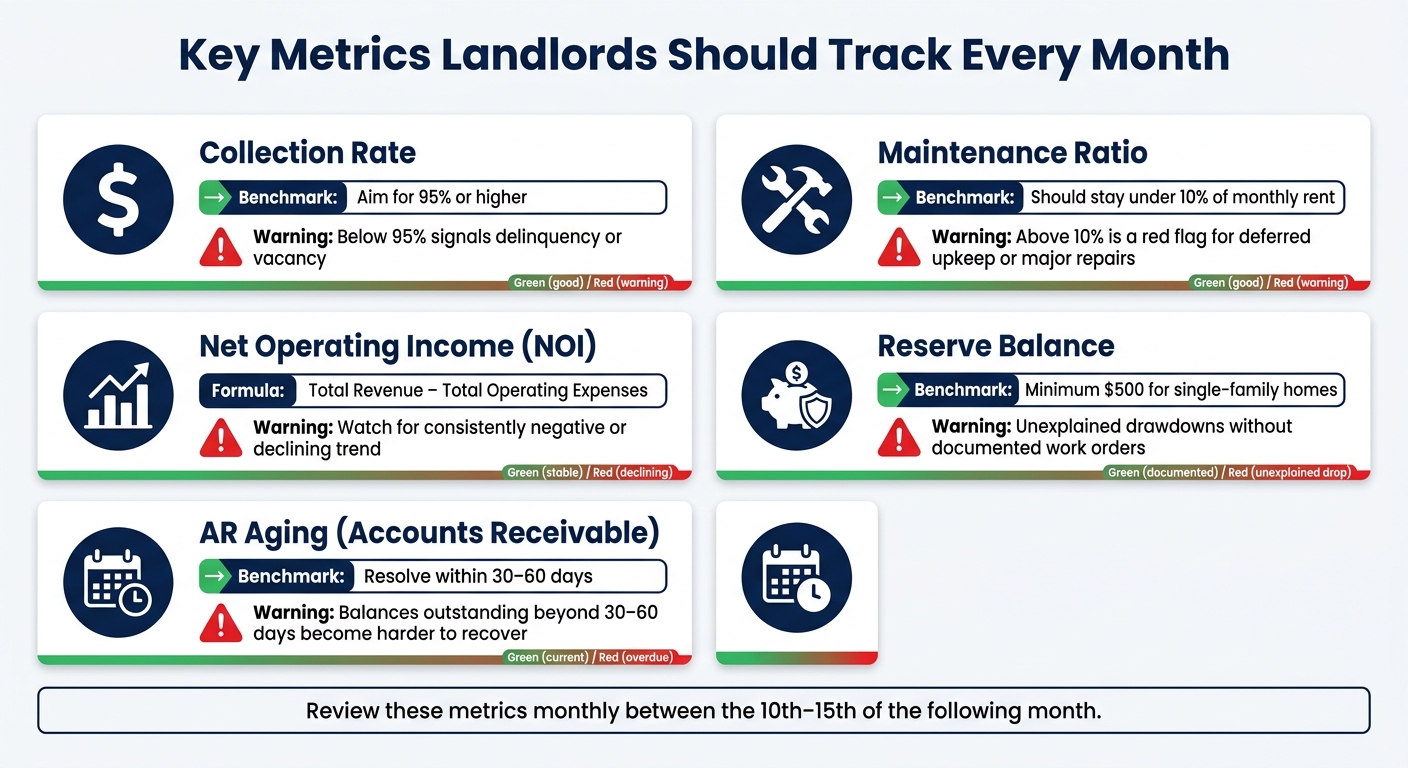

Key Metrics Landlords Should Track Each Month

Key Metrics Landlords Should Track Monthly

Keeping an eye on specific metrics can help uncover issues that might be buried in raw data. These figures not only highlight potential problems but also guide you in taking corrective steps.

Gross Scheduled Rent vs. Collected Rent

Gross Scheduled Rent (GSR) represents the total rent your property should bring in if every unit is occupied and tenants pay in full. On the other hand, Collected Rent is the actual amount deposited into your account. The difference between these two is your collection rate – and it’s a crucial indicator.

A collection rate under 95% is a warning sign. This could point to vacant units, delinquent tenants, or even unnoticed partial payments. If collected rent falls short of expectations, use your rent roll and Accounts Receivable (AR) report to track overdue balances – whether they’re 30, 60, or 90+ days past due. The longer a balance remains unpaid, the harder it becomes to recover, especially after the 30-to-60-day window.

"Profit on paper is great, but cash in hand is what pays the bills." – RentRedi

Comparing GSR to collected rent can also reveal if long-term tenants are paying far below market rates. This gap grows over time, eating into your potential revenue until adjustments are made.

Once you’ve assessed rent collection, shift focus to managing expenses and monitoring profitability.

Operating Expenses and Net Operating Income

After reviewing rent figures, turn your attention to expenses to ensure a healthy Net Operating Income (NOI). NOI is the clearest indicator of your property’s profitability. The formula is simple: total revenue minus total operating expenses. These expenses include management fees (usually 8%–12% of collected rent in Jacksonville), maintenance, taxes, insurance, and other related costs.

If maintenance expenses exceed 10% of monthly rent, it could signal deferred upkeep or looming major repairs. Tracking NOI month by month, along with a Year-to-Date (YTD) column, can help you spot whether a spike is a one-off event or part of a larger trend.

"Most property owners don’t lose money overnight. They lose it slowly by failing to review the right reports regularly." – Crystal Abing, Director of Content Marketing, RentRedi

For better insights, maintain separate profit-and-loss (P&L) statements for each property. This approach makes it easier to identify underperforming assets.

Reserve Balances and Capital Expenditure Tracking

In addition to monitoring daily income and expenses, it’s essential to keep an eye on reserve balances and distinguish between routine repairs and capital expenditures (CapEx). Your reserve balance isn’t just a safety net – it’s a key metric to review each month. Reports should clearly show the starting balance, any withdrawals, and the ending balance. If reserves drop unexpectedly (for example, from $500 to $120 without a documented work order), it’s time to investigate.

Equally important is how expenses are categorized. Routine repairs count as operating expenses and are deductible in the year they occur. However, Capital Expenditures (CapEx) – like replacing a roof or upgrading appliances – must be depreciated over 27.5 years for tax purposes. Keeping these categories separate from the beginning simplifies year-end accounting and ensures accurate monthly NOI calculations.

| Metric | What to Watch For |

|---|---|

| Collection Rate | Below 95% signals delinquency or vacancy |

| Maintenance Ratio | Above 10% of monthly rent is a red flag |

| Net Operating Income | Consistently negative or declining trend |

| Reserve Balance | Unexplained drawdowns without documentation |

| AR Aging | Balances outstanding beyond 30–60 days |

Best Practices for Organizing and Reviewing Reports

Organizing Reports by Property and Year

Keeping your financial reports organized by property and labeled by date is one of the easiest ways to maintain clarity. Label each monthly statement with the property name and the month/year (e.g., "Oak Street Duplex / 05/2026"). This method allows you to quickly locate data when needed. It’s especially important to keep financials for each property separate. Why? Because a high-performing property can hide issues with a weaker one, and by the time you notice, it might be too late.

For landlords managing multiple properties, a consolidated portfolio summary offers a helpful overview. However, it’s essential to maintain individual profit and loss (P&L) statements for each property beneath that summary. This separation not only provides clarity but is also critical for accurate tax reporting at the end of the year.

"You can’t manage what you can’t measure." – 1 Realty Management

Monthly Review Checklist

When your reports arrive – ideally between the 10th and 15th of the following month – follow a consistent review process. Begin with the P&L statement to determine whether the property was profitable or not. Next, compare the rent roll to your bank deposits to ensure all collected rent is accounted for. Then, review the Accounts Receivable (AR) aging report to identify any tenant balances overdue by more than 30 days.

Make sure to reconcile reserve drawdowns with documented work orders and check Accounts Payable to confirm that mortgages, utilities, and vendor invoices are up to date. Finally, review lease end dates – leases expiring in the next 60–90 days need your attention sooner rather than later. By sticking to this routine, you’ll set yourself up for a smoother tax season and fewer headaches.

Using Reports for Tax Preparation

Consistently reviewing your reports each month doesn’t just improve day-to-day management – it also simplifies tax preparation. The most important habit here is categorizing expenses consistently throughout the year. Organize costs into clear categories like maintenance, insurance, property taxes, management fees, and utilities. This ensures your records align with IRS Schedule E requirements when it’s time for your CPA to step in.

One critical distinction to keep in mind: routine repairs are fully deductible in the year they occur, while capital improvements (like installing a new HVAC system or replacing a roof) must be depreciated over 27.5 years. Misclassifying these expenses can inflate your net operating income (NOI) and cause complications when filing. To avoid this, digitally attach invoices and receipts to transactions as they happen. This creates a ready-to-go audit trail without requiring extra effort at year-end.

Jacksonville-Specific Reporting Considerations

Tracking Property Tax and Insurance in Coastal Florida

Owning rental properties in Florida comes with unique challenges, particularly when it comes to property taxes and insurance. Unlike primary residences, rental properties in Florida don’t benefit from homestead exemptions. This means you’ll face higher non-homestead tax rates. In Jacksonville, property taxes typically range from 1% to 1.5% of the assessed value annually. Since rates can vary by neighborhood, it’s essential to get detailed tax estimates for each property you own.

Insurance is another area where coastal properties can complicate budgeting. Locations like Jacksonville Beach, Ponte Vedra, and Atlantic Beach are prone to higher premiums due to increased windstorm and flood risks. On average, standard landlord insurance costs between $1,000 and $2,000 per year, but coastal properties often require additional coverage, which can significantly impact your bottom line. For instance, an extra $200 per month in premiums translates to a $2,400 annual reduction in cash flow.

"Policies written at 2022 or 2023 replacement values may no longer reflect current rebuilding costs." – CrossView Property Management

Given the rising costs of construction and labor in Northeast Florida, an annual insurance review is highly recommended to ensure your coverage limits are adequate. Combined with taxes, these expenses can make a big dent in your annual budget, so staying proactive is key.

Seasonal Trends in Jacksonville Rentals

Jacksonville’s rental market experiences predictable seasonal shifts that directly affect operating costs and tenant turnover. Late spring and early summer are particularly active, with higher rates of tenant turnover during these months. This often leads to increased spending on make-ready expenses like cleaning and repairs, which can range from $1,500 to $4,000 per vacancy.

The summer months also bring additional challenges, such as increased HVAC repairs and pest control needs, driven by the region’s heat and humidity. Scheduling preventative HVAC maintenance in the spring can help avoid costly surprises during peak summer. On the other hand, winter tends to be slower for the rental market, so it’s wise to start marketing vacant units 45 to 60 days before a lease ends to minimize downtime. Local factors, like military transfer cycles at Naval Air Station Jacksonville and student turnover, also contribute to fluctuations in demand.

Seasonal costs and tenant behavior are just part of the equation. Navigating Florida’s regulatory landscape is another critical aspect of managing Jacksonville rentals.

Compliance with Florida Rental Laws

Florida rental laws come with specific requirements that landlords must account for in their financial reporting. For example, security deposits must be held in separate interest-bearing accounts or covered by a surety bond. Additionally, landlords are required to document statutory fees, such as the $50 charge for issuing 3-day pay-or-quit or 7-day cure notices. If you’re an out-of-state property owner, don’t forget to account for the $50/year registered statutory agent fee, which should be recorded as a monthly expense.

"In a market shaped by storm risk, insurance pressure, and rising service costs, owners need reporting that goes beyond mere numbers." – Blakely Hughes, Broker, Nest Finders

To simplify compliance, firms like 1 Realty Management integrate Florida-specific legal requirements into their financial reporting processes. This approach helps Jacksonville landlords stay compliant without the need for constant follow-ups, ensuring smoother operations in a challenging market.

Conclusion: Using Monthly Reports to Manage Your Rental Portfolio

The Case for Professional Reporting

Monthly reports are essential for understanding how your property is performing. Metrics like Net Operating Income (NOI) and reserve balances highlight the value of tracking measurable performance indicators.

"Bank reconciliation and systematic record-keeping mean your financials are accurate, consistent, and audit-ready at any point in time." – 1 Realty Management

Professional reporting takes this to the next level. Backed by 45 years of experience in the Jacksonville rental market, 1 Realty Management provides reports that meet Florida-specific compliance needs. These include trust account tracking and legal notice documentation, ensuring your records are ready for tax season and audits. With accurate financial data at your fingertips, you can make quick, well-informed decisions.

Next Steps for Landlords

Use these insights to establish a routine for reviewing your reports. Aim to review monthly statements promptly after receiving them to address any discrepancies early. Pay close attention to three numbers: your Net Operating Income (NOI), reserve balance, and outstanding accounts receivable. These figures can give you an immediate sense of whether the month met your expectations or requires further action.

If your current reports are unclear, delayed, or incomplete, it may be time to reevaluate your reporting system. Accurate, timely, and detailed reporting isn’t just a nice-to-have – it’s a fundamental part of effective property management. Partner with a team that prioritizes financial transparency to protect and grow your investment.

FAQs

How do I reconcile my rent roll with my bank deposits?

To reconcile your rent roll with bank deposits, start by comparing the tenant payments recorded in your accounting ledger to the actual funds shown in your bank statement. Match the payments listed on your rent roll – which outlines expected payments and their statuses – with the deposits reflected in your account. Double-check that the total cash inflows, minus any verified outflows, align with your bank’s closing balance. Keeping up with this process regularly ensures your records stay accurate and simplifies things when it’s time to handle taxes.

What’s the fastest way to spot errors or missing charges in my monthly statement?

To spot errors or missing charges efficiently, compare your monthly statement with your property management agreement and the original invoices. Make sure fees align with your contract, and check that maintenance items list the vendor’s name, a description of the work, and the invoice details. Use real-time data from your owner portal to cross-check the statement. If something doesn’t add up or seems unusual, reach out to your property manager for clarification.

How can I tell if an expense should be categorized as a repair or CapEx?

When deciding whether an expense is a repair or a capital expenditure (CapEx), the key is to think about whether it restores or improves the property.

- Repairs: These bring the property back to its original condition, like patching a leak or fixing a broken window. They’re considered deductible expenses in the year they occur.

- CapEx: These go beyond simple fixes – they add value, extend the life of the property, or involve major upgrades. For example, replacing an entire roof or installing a new HVAC system would fall into this category. Instead of deducting these costs immediately, they’re depreciated over time.

To keep everything clear, make sure your monthly statements clearly separate routine maintenance from larger, one-time expenses. This will help you stay organized and avoid confusion when it’s time to file taxes.