Financial reporting is a critical part of managing apartment properties effectively. It helps track income, expenses, and cash flow, ensuring you make informed decisions and stay compliant with tax regulations. The three main financial statements every apartment owner needs to understand are:

- Income Statement (Profit and Loss Statement): Tracks rental income and operating expenses over time. Key metric: Net Operating Income (NOI).

- Balance Sheet: Provides a snapshot of your property’s financial position, detailing assets, liabilities, and owner’s equity.

- Cash Flow Statement: Shows how money moves in and out of your accounts, categorized into operating, investing, and financing activities.

Additionally, organizing transactions using a Chart of Accounts (COA) simplifies financial tracking by grouping income and expenses into clear categories. Properly categorizing repairs, capital improvements, and management fees ensures accurate reporting and tax preparation.

Consistent documentation, separate bank accounts for operating funds, security deposits, and reserves, along with monthly reconciliations, are key practices for maintaining financial clarity. Accurate financial reporting not only helps you monitor profitability but also builds trust with lenders, investors, and stakeholders.

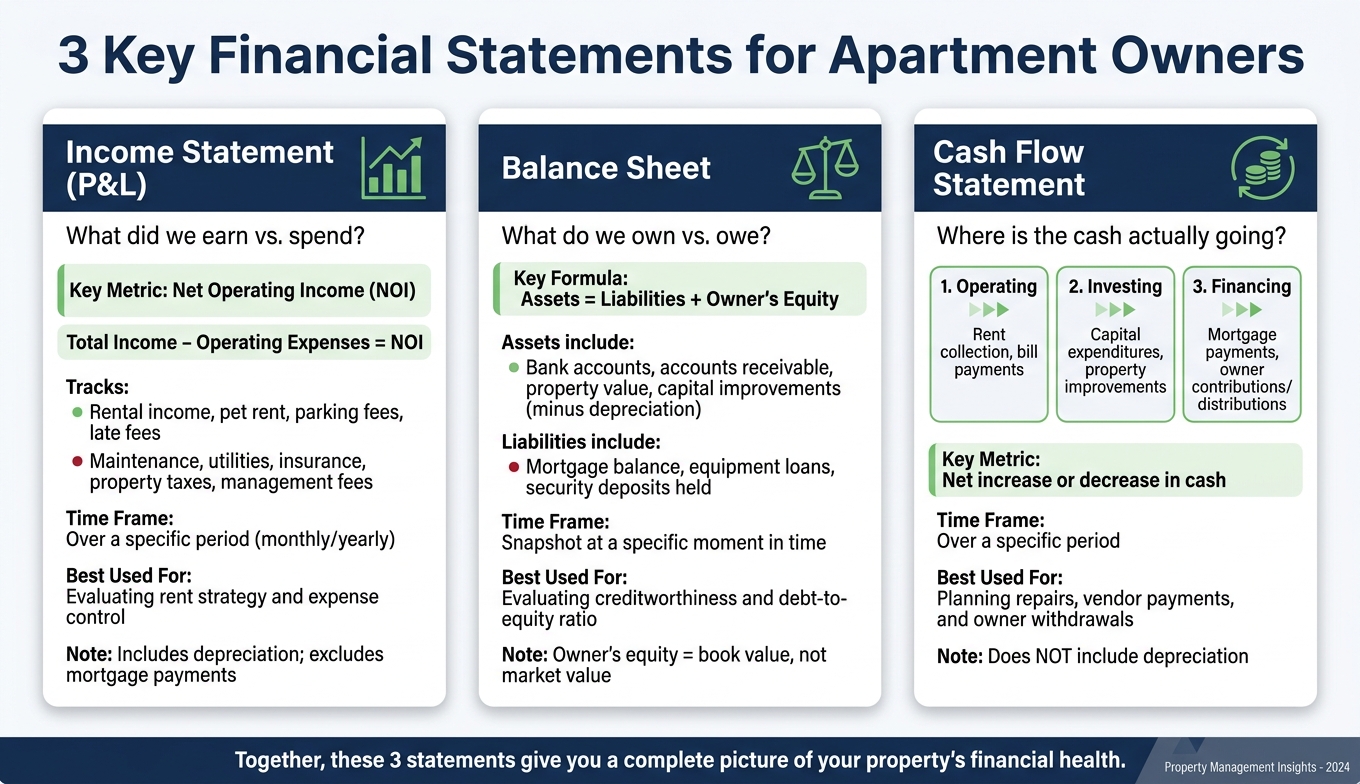

Key Financial Statements Every Apartment Owner Should Know

3 Key Financial Statements for Apartment Owners: At a Glance

Three key documents form the backbone of financial reporting for apartment owners. Each of these statements answers a distinct question about your property’s financial health, and together, they provide the insights needed to make informed decisions. Let’s break down the role of each.

Income Statements

The income statement – often referred to as a Profit and Loss (P&L) statement – details your rental income and operating expenses over a specific period, giving you a clear picture of your property’s profitability. Income sources typically include base rent, pet rent, late fees, parking fees, and application fees. On the expense side, you’ll see items like maintenance, utilities, insurance, property taxes, and management fees.

“A profit and loss (P&L) statement, sometimes called an income statement, shows your rental income minus your operating expenses. This calculation gives you the net operating income (NOI), a key metric for understanding a property’s profitability.” – Jake Belding, Content Marketing Specialist, Buildium

At the heart of the P&L is the Net Operating Income (NOI) – the amount left after subtracting operating expenses from total income. This figure excludes mortgage payments and major capital projects, offering a snapshot of your property’s core profitability. Regularly comparing P&L statements (monthly or yearly) can help you spot trends, like sudden increases in repair costs or income fluctuations, that may need attention.

It’s important to note that major upgrades, such as a roof replacement, should not be listed as regular repairs on the P&L. These are categorized as capital improvements and depreciated over time, a distinction that plays a crucial role during tax season.

While the Income Statement shows performance over time, the Balance Sheet provides a real-time snapshot of your property’s financial standing.

Balance Sheets

The balance sheet offers a snapshot of what your property business owns, owes, and is worth at a specific moment. It operates on a straightforward formula:

Assets = Liabilities + Owner’s Equity

Assets include items like operating bank accounts, accounts receivable (unpaid rent), the property itself, and capital improvements, minus accumulated depreciation. Liabilities cover obligations such as your mortgage balance, equipment loans, and security deposits held – a critical line item since these funds are owed back to tenants. The difference between assets and liabilities is the owner’s equity.

Lenders use the balance sheet to evaluate your creditworthiness and debt-to-equity ratio before approving financing. However, keep in mind that “owner’s equity” represents the book value of your property, not its current market value. This distinction is important when assessing your property’s worth.

Cash Flow Statements

The cash flow statement tracks the actual movement of money into and out of your accounts. Unlike the income statement, which might show a profit on paper, the cash flow statement reveals how much money is immediately available.

It organizes cash activity into three categories:

- Operating: Day-to-day activities like collecting rent and paying bills.

- Investing: Capital expenditures and property improvements.

- Financing: Mortgage payments, owner contributions, or distributions.

This breakdown is especially useful for planning owner withdrawals, timing major repairs, and ensuring you maintain sufficient reserves. When combined with the Income Statement and Balance Sheet, the Cash Flow Statement gives you a complete view of your property’s financial health.

| Feature | Income Statement (P&L) | Cash Flow Statement |

|---|---|---|

| Primary Focus | Profitability over a period | Actual cash movement |

| Key Metric | Net Operating Income (NOI) | Net increase or decrease in cash |

| Includes Depreciation? | Yes | No |

| Best Used For | Evaluating rent strategy and expense control | Planning repairs, vendor payments, and owner draws |

sbb-itb-73b3b1a

Chart of Accounts for Apartment Owners

The chart of accounts is a cornerstone for detailed financial reporting, transforming raw data into actionable insights. A chart of accounts (COA) categorizes every financial transaction into five main groups: Assets, Liabilities, Equity, Income, and Expenses. This structure not only ensures precise financial reporting but also supports the accounting processes that follow.

To keep things organized, use a hierarchical numbering system with a parent-child format. For instance, you might list “Utilities” as a parent account with subaccounts like Electric, Water, and Gas. Revenue accounts could fall within the range of 4000–4999, while Expense accounts might be numbered 5000–5999.

“Having a clear, concise chart of accounts is crucial for your clients to understand how their rental properties are performing. It can guide future investments and help both you and your clients make important financial decisions.” – Taylor Brugna, Partner at The Real Estate CPA

Rental Income Categories

Your income accounts should reflect every revenue stream your property generates – not just base rent. Typical subaccounts might include monthly rent, pet rent, parking fees, laundry income, storage fees, late fees, and application fees. For non-refundable lease initiation fees, instead of recording them as immediate income, amortize them over the lease term.

If you own multiple properties, consider assigning property-specific codes to each account. For example, 4101 could represent Rent at Property A, while 4102 might track Rent at Property B. This method allows you to view consolidated portfolio reports while still monitoring individual property performance.

While income accounts focus on revenue, properly categorizing expenses is just as crucial.

Operating Expense Categories

Operating expenses include the everyday costs of managing your property. These typically cover repairs, landscaping, pest control, cleaning, HVAC servicing, plumbing, electrical work, and trash collection. For multi-family properties, operating expenses usually range between 35% and 45% of gross rental income, a useful benchmark for evaluating your own costs. Investors looking for strong returns often look to Westside Jacksonville property management to optimize these margins.

It’s important to distinguish repairs from capital improvements. For instance, fixing a leaky faucet is an operating expense, recorded immediately. However, replacing an entire roof is a capital expenditure, which should be capitalized and depreciated over time. Misclassifying these can distort your Net Operating Income (NOI) and lead to tax complications. Additionally, avoid overusing a “Miscellaneous” account – it can obscure spending patterns and make trend analysis difficult.

For further clarity, management fees and administrative costs should be tracked in their own distinct accounts.

Management Fees and Administrative Costs

Management fees and administrative costs should be recorded separately from general operating expenses.

“A detailed chart of accounts that separates rental income, repairs, utilities, management fees and capital expenses enables GAAP‑compliant tracking at the property level.” – Vittoria “Torri” Heggie, James Moore

Management fee accounts should include the base fee, leasing commissions, and any maintenance markups. Administrative subaccounts, on the other hand, might cover software subscriptions, legal fees, accounting services, advertising, and office supplies. Keeping these costs separate from property expenses helps clarify where money is being spent and whether your management arrangement is providing good value.

Core Accounting Processes for Apartment Owners

Having a well-organized chart of accounts is just the beginning. To ensure your financial reports are accurate and useful, you need to follow key accounting processes. Consistent tracking and recording turn your structured accounts into dependable financial insights.

Recording Transactions

Every transaction needs to be recorded in a general journal, including the date, affected accounts, amounts, and a brief description. From there, entries are posted to a general ledger using double-entry bookkeeping. This method records each transaction as both a debit and a credit, which helps maintain running balances and catch errors. At the end of the month, reconcile your records with your bank statements to identify typos, duplicate entries, or bank errors.

Your accounting method also plays a role. Cash accounting records income and expenses when money changes hands, making it straightforward for smaller operations. Accrual accounting, on the other hand, records transactions when they occur, offering a better view of your financial position and aligning with GAAP standards.

These detailed records are the foundation for calculating key metrics like Net Operating Income (NOI).

Calculating Net Operating Income (NOI)

NOI measures how well your property performs as a business. It’s calculated by subtracting operating expenses from total revenue, excluding costs like mortgage payments, capital expenditures, depreciation, and taxes.

“Every dollar of NOI you add – through higher rents, lower vacancy, or reduced operating costs – directly increases what the property is worth.” – REI Prime

NOI also plays a critical role in property valuation. Using the formula:

Property Value = NOI ÷ Capitalization Rate,

an increase in NOI leads to a higher asset value. Lenders also use NOI to determine the Debt Coverage Ratio (DCR), ensuring the property generates enough cash flow to meet its debt obligations.

Tracking Depreciation and Deductible Expenses

Keeping track of depreciation and deductible expenses is essential for maximizing tax benefits. Depreciation provides a major tax advantage for apartment owners. Under the Modified Accelerated Cost Recovery System (MACRS), residential rental properties can be depreciated over 27.5 years using a straight-line method, though land itself cannot be depreciated.

“Depreciation is the single most valuable deduction for rental property owners, allowing you to recover the cost of your property over 27.5 years even while the property appreciates in market value.” – Madras Accountancy

Depreciation begins when the property is “placed in service”, meaning it’s ready for rent – even if no tenant has moved in yet . The first-year deduction is based on the month the property is placed in service .

Additionally, keep a detailed record of deductible operating expenses like management fees, repairs, insurance premiums, professional fees, and owner-paid utilities. Routine repairs can be deducted immediately, but improvements that extend the property’s life must be capitalized and depreciated over time . Save documentation like dated photos and receipts to prove whether an expense qualifies as a repair or an improvement, especially in case of an IRS audit.

Best Practices for Accurate Financial Reporting

Accurate financial reporting hinges on disciplined practices, starting with well-organized funds and consistent monthly reporting. Even the best accounting systems won’t deliver reliable results without a solid framework. Building strong habits is key to producing financial reports that inspire confidence rather than raise doubts.

Using Dedicated Bank Accounts

Keeping funds in separate accounts is essential. Ideally, you should maintain three distinct accounts: one for operating funds, one for tenant security deposits, and one for capital reserves. Mixing tenant deposits with operating funds – known as commingling – not only complicates accounting but can also lead to legal trouble.

“Mixing these trust funds with your operating account creates what’s called commingling. Commingling violates state regulations and can result in losing your property management license.” – Jake Belding, Buildium

Segregating funds reduces legal risks and simplifies monthly reconciliations. For best results, aim to complete reconciliations by the 3rd business day of each month. This ensures that your financial statements are based on verified data.

| Account Type | Purpose | Key Requirement |

|---|---|---|

| Operating Account | Day-to-day revenue and expenses | Contains only property-related income and costs |

| Security Deposit/Trust | Tenant deposits held for the lease period | Must remain separate from operating funds; often legally required |

| Reserve Account | Funds for major capital expenditures | Used for long-term improvements like roof replacements or HVAC upgrades |

By assigning specific purposes to each account, you can streamline reconciliations and ensure accurate reporting for property owners.

Generating Monthly Owner Reports

Consistent monthly owner reports are vital for keeping stakeholders informed about property performance. A well-rounded report should include gross income, operating expenses, net operating income (NOI), and cash flow. Using a standardized template allows for easier comparisons across periods.

To provide context, include a variance narrative that explains any deviations from the budget. For example: “Turn costs increased due to five unexpected move-outs.” Without this explanation, a spike in expenses might seem alarming; with it, the report becomes more transparent. A structured monthly close calendar can help you stay on track: complete reconciliations by day 3, prepare variance notes by day 5, and distribute the report by day 6.

“Property managers don’t lose clients because the grass wasn’t cut or the rent wasn’t collected. They lose them because they can’t answer simple money questions fast enough.” – Swara, Property Management Technology Consultant

In addition to detailed reporting, staying compliant with tax regulations is equally important.

Meeting IRS Compliance Requirements

When reporting rental income and expenses, use Schedule E (Form 1040). If you pay a vendor – like a plumber, landscaper, or handyman – $600 or more in a calendar year, you’ll need to issue a Form 1099-NEC for non-employee compensation. To prepare, flag vendors once their payments reach $400. This gives you time to collect a W-9 before hitting the reporting threshold.

Security deposits also require careful handling. Failing to return them within the required timeframe can lead to penalties and legal fees. Maintaining a security deposit ledger that aligns with your trust account balance protects you legally and ensures your records are audit-ready.

At 1 Realty Management, these practices are part of our financial reporting approach, ensuring both compliance and transparency for your property.

Conclusion

Financial reporting is essential for maintaining clarity and confidence when managing your apartment property. As the Rentable Team aptly states, “Accounting is at the heart of effective property management… it’s what drives financial health and long-term growth.”

Your income statement, balance sheet, and cash flow statement each reveal a unique aspect of your property’s financial story. Together, they help you understand the difference between theoretical profit and actual cash on hand, identify trends early, and make informed decisions about pricing, maintenance, and growth opportunities. These statements not only guide your strategic choices but also help protect your business from potential regulatory pitfalls.

Accurate and well-maintained records are your legal and financial safety net. They ensure compliance with IRS requirements, proper 1099 filings, and adherence to security deposit regulations. Keeping digital or printed copies of your financial statements for at least five years is a smart practice to support audits or resolve legal issues.

“An accurate statement isn’t just for recordkeeping, it’s a management tool.” – Hostaway

If managing financial reporting feels overwhelming, professional help can make all the difference. For those managing apartment properties in Jacksonville, FL, 1 Realty Management provides full-service financial reporting as part of their property management solutions. With their expertise, you can rest assured your numbers are accurate, well-organized, and always ready when needed.

FAQs

How do I know if an expense is a repair or a capital improvement?

An expense qualifies as a repair when it simply keeps the property in its usual condition without noticeably boosting its value or extending its lifespan. On the other hand, it’s considered a capital improvement if it enhances the property’s value, prolongs its useful life, or modifies it for a different use. The IRS relies on the Betterment, Adaptation, and Restoration (BAR) framework to make this distinction.

Why does my P&L show profit but my bank balance is low?

Your Profit and Loss (P&L) statement may show a profit because it tracks income and expenses when they are earned or incurred, not when cash actually changes hands. A low bank balance, on the other hand, could be due to timing differences in cash flow. For example, you might have unpaid invoices, upcoming expenses, or recent payments that haven’t cleared yet. This underscores why keeping an eye on both cash flow and profit is crucial to understanding your financial health.

What accounts should I separate for an apartment property?

To keep your financial records organized, create separate accounts for the current rent roll, operating expenses, assets, liabilities, and equity tied to the apartment property. This approach makes it easier to track and report your property’s finances accurately.